All Categories

Featured

Table of Contents

You may be asked to make additional premium settlements where insurance coverage can terminate since the rate of interest rate dropped. Your starting rates of interest is fixed only for a year or in many cases 3 to 5 years. The assured rate offered in the plan is a lot reduced (e.g., 4%). One more feature that is sometimes stressed is the "no expense" lending.

In either instance you need to obtain a certificate of insurance defining the stipulations of the team policy and any insurance fee - which of the following is not a characteristic of term life insurance?. Typically the optimum quantity of insurance coverage is $220,000 for a home loan and $55,000 for all other debts. Credit life insurance policy need not be bought from the organization giving the financing

Accidental Death Insurance Vs Term Life

If life insurance is needed by a financial institution as a problem for making a finance, you might have the ability to assign an existing life insurance plan, if you have one. However, you may desire to purchase team credit history life insurance despite its higher price due to its benefit and its availability, usually without in-depth proof of insurability.

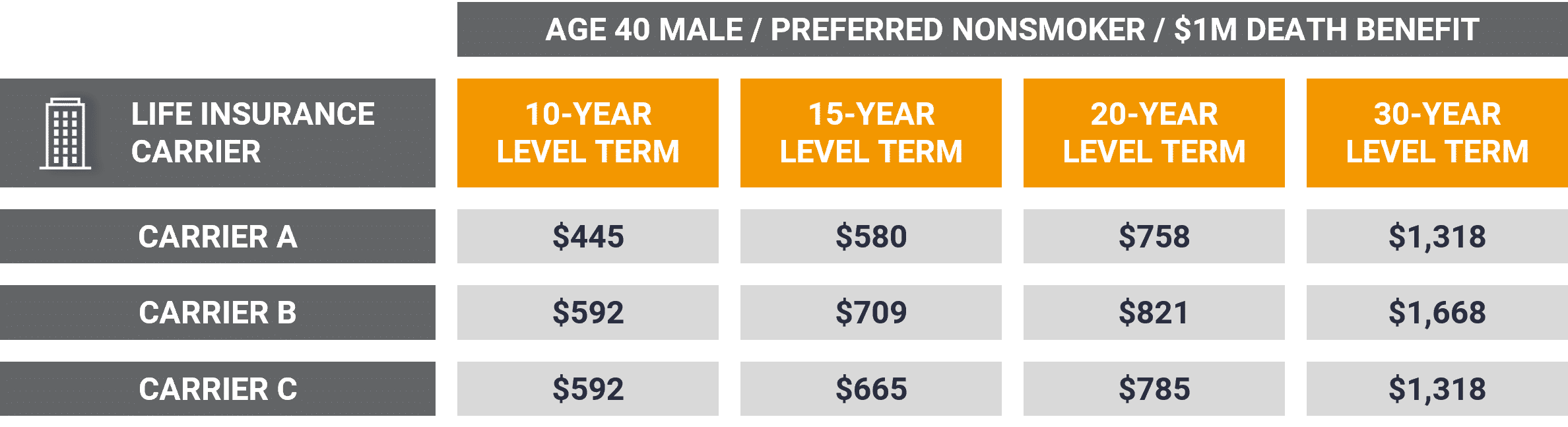

Nevertheless, home collections are not made and premiums are sent by mail by you to the representative or to the business. 10 year renewable term life insurance. There are particular elements that have a tendency to raise the expenses of debit insurance policy more than regular life insurance coverage strategies: Particular expenses are the exact same regardless of what the dimension of the policy, to make sure that smaller plans released as debit insurance policy will have greater premiums per $1,000 of insurance policy than larger dimension routine insurance policies

Does Term Life Insurance Have Living Benefits

Considering that very early gaps are costly to a firm, the prices need to be passed on to all debit policyholders. Given that debit insurance is made to include home collections, higher payments and charges are paid on debit insurance policy than on normal insurance policy. In most cases these higher expenditures are passed on to the insurance holder.

Where a company has different costs for debit and regular insurance policy it may be possible for you to purchase a larger quantity of regular insurance policy than debit at no added expense. If you are assuming of debit insurance, you must certainly investigate normal life insurance coverage as a cost-saving choice.

This strategy is made for those that can not at first afford the normal whole life costs but who want the greater premium coverage and feel they will become able to pay the greater premium - term life insurance with critical illness rider. The family members plan is a mix strategy that offers insurance protection under one agreement to all participants of your immediate household partner, wife and children

Joint Life and Survivor Insurance provides protection for two or even more individuals with the death advantage payable at the death of the last of the insureds. Premiums are substantially lower under joint life and survivor insurance than for policies that insure just one person, since the possibility of needing to pay a death insurance claim is lower.

Premiums are considerably more than for plans that guarantee one person, given that the chance of needing to pay a fatality case is greater - term life insurance vs universal life insurance. Endowment insurance coverage supplies for the settlement of the face quantity to your recipient if fatality takes place within a certain period of time such as twenty years, or, if at the end of the particular duration you are still alive, for the repayment of the face total up to you

{kind=link}

Latest Posts

Level Term Life Insurance Uk

Term Life And Ad&d Insurance

What Does 15 Year Term Life Insurance Mean